The Fed held rates steady at 3.50–3.75% yesterday, but their forward guidance is basically signaling another hike before year-end. According to Reuters coverage of the decision, officials are pointing toward at least one more increase, which means inventory financing costs are about to climb again.

Last week I was helping a distributor in Phoenix restructure their inventory strategy ahead of this. Their line of credit was already costing an extra $2,800 per month compared to eighteen months ago. Another rate bump adds potentially another thousand monthly just to maintain the same stock levels.

Most small businesses are carrying way too much inventory for this interest rate environment. Stocking strategies got built when money was cheap. Now those same strategies are bleeding cash through carrying costs that compound every day.

The hidden multiplier effect

Your actual inventory carrying cost isn't just the interest rate on your credit line. That's the mistake I see constantly—businesses looking at their 8.5% business line of credit and treating that as the full picture.

The real number is usually 20–25% annually when you factor everything in.

When rates go up, your credit line gets more expensive, obviously. But you're also paying more for warehouse space because your landlord's financing costs went up. Insurance premiums climb. Utility costs spike. It compounds across every expense line tied to borrowing.

A furniture retailer I worked with last month discovered their true carrying cost had jumped from 18% to 24% over two years. On $800k of average inventory, that's roughly $48,000 annually just gone. They had no idea until we mapped it out.

The worst part? Most businesses respond by trying to negotiate better prices with suppliers. But suppliers are facing the same pressure, so they're extending payment terms instead of cutting prices. Now you're financing their inventory too.

Why traditional inventory metrics fall apart here

Businesses are still using reorder points and safety stock calculations they set up years ago. Those formulas assume carrying costs are relatively stable. They're not.

Never run out of stock or overorder again.

Listoly streamlines inventory workflows to keep your business stocked and profitable.

- Real-time stock tracking

- Automated reorder alerts

- Supplier and purchase management

No credit card required

Your economic order quantity calculation probably uses a carrying cost percentage that hasn't been updated since 2019. Every inventory management textbook teaches EOQ with a static carrying cost input. In this environment, that number should be recalculated quarterly at minimum.

A specialty food distributor nearly went under because they kept ordering based on volume discounts that made sense at 15% carrying costs but destroyed cash flow at 23%. They were saving 8% on purchase price and losing 12% on carrying costs—a net loss on every deal they thought they were winning.

Standard safety stock formulas are even worse. They optimize for service level without accounting for the financing cost of that buffer. A 98% service level might have made sense when money was cheap. At current rates, dropping to 95% on C-items could free up enough cash to cover two months of interest payments.

The businesses surviving this are treating carrying cost as a variable input, not a constant. They're recalculating everything—reorder points, safety stock, which SKUs to keep—based on current financing costs.

Building your rate-adjusted inventory playbook

The approach that actually works starts with segmenting your inventory by financing method. Not ABC analysis—that's about velocity. This is about how each chunk of inventory hits your borrowing.

Inventory financing segments:

Start by identifying what's bought on credit versus supplier terms. Inventory on your credit line is costing you the full interest rate. Inventory on net-30 or net-60 terms is essentially free financing if you're paying on time.

Then look at what's pre-sold versus speculative stock. Pre-sold inventory with customer deposits has negative carrying cost—customers are financing it for you. Speculative stock carries the full burden plus risk.

Finally, separate seasonal from evergreen items. Seasonal inventory might only incur 3–4 months of carrying costs if you time it right. Evergreen items sitting for nine months are a slow drain.

A building supplies company cut their interest expense by around $4,100 monthly just by restructuring which items they finance through which mechanism. They moved slow-movers to consignment, pushed suppliers for longer terms on predictable items, and reserved their credit line for fast-turning stock with confirmed demand.

The 72-hour cash recovery assessment

Forget complex modeling for a minute. Walk your warehouse or stockroom with one question: if you had to raise $50k in 72 hours, what inventory would you liquidate?

Whatever you identify probably shouldn't be there at these interest rates. If your first instinct in a cash crunch is to dump it, why are you paying 8–10% annually to store it?

Most businesses surface the same patterns pretty quickly:

-

Duplicate SKUs customers don't actually distinguish between

-

Old promotional inventory from campaigns that didn't work

-

Safety stock on items with reliable 3-day supplier delivery

-

Premium versions of products where the basic version outsells 10

1

-

Seasonal items held "just in case" for off-season orders

Prioritize liquidation of SKUs with the highest monthly carrying cost per dollar of inventory.

One electronics retailer found $120k worth of inventory in this exercise. They cleared it at 70 cents on the dollar, took the margin hit, and saved roughly $1,900 per month in carrying costs. The margin hit was recovered through reduced interest expense within eight months.

Renegotiating supplier terms

Everyone asks for better payment terms when cash gets tight. That's obvious. The real opportunity is restructuring how inventory ownership transfers.

Consignment arrangements make more sense now than they did a few years ago. Larger suppliers often have access to cheaper capital than you do. Propose a consignment model where you pay only when items sell. Even if they charge a 5% premium, you're ahead when your carrying cost is 20%+.

Vendor-managed inventory is another underused option. Let suppliers own the inventory until you need it—they handle the carrying cost, you handle the sales. A hardware store chain I work with shifted about 30% of their inventory to VMI and freed up roughly $200k in working capital.

Frame it as partnership, not desperation. You're offering better demand visibility and guaranteed shelf space in exchange for inventory financing. Suppliers with strong balance sheets often prefer this—it locks in customer relationships when credit is tight.

Floor planning arrangements aren't just for auto dealerships either. Furniture stores, equipment dealers, and some electronics retailers use this model. Any high-value inventory can potentially be floor-planned where the supplier retains ownership until point of sale.

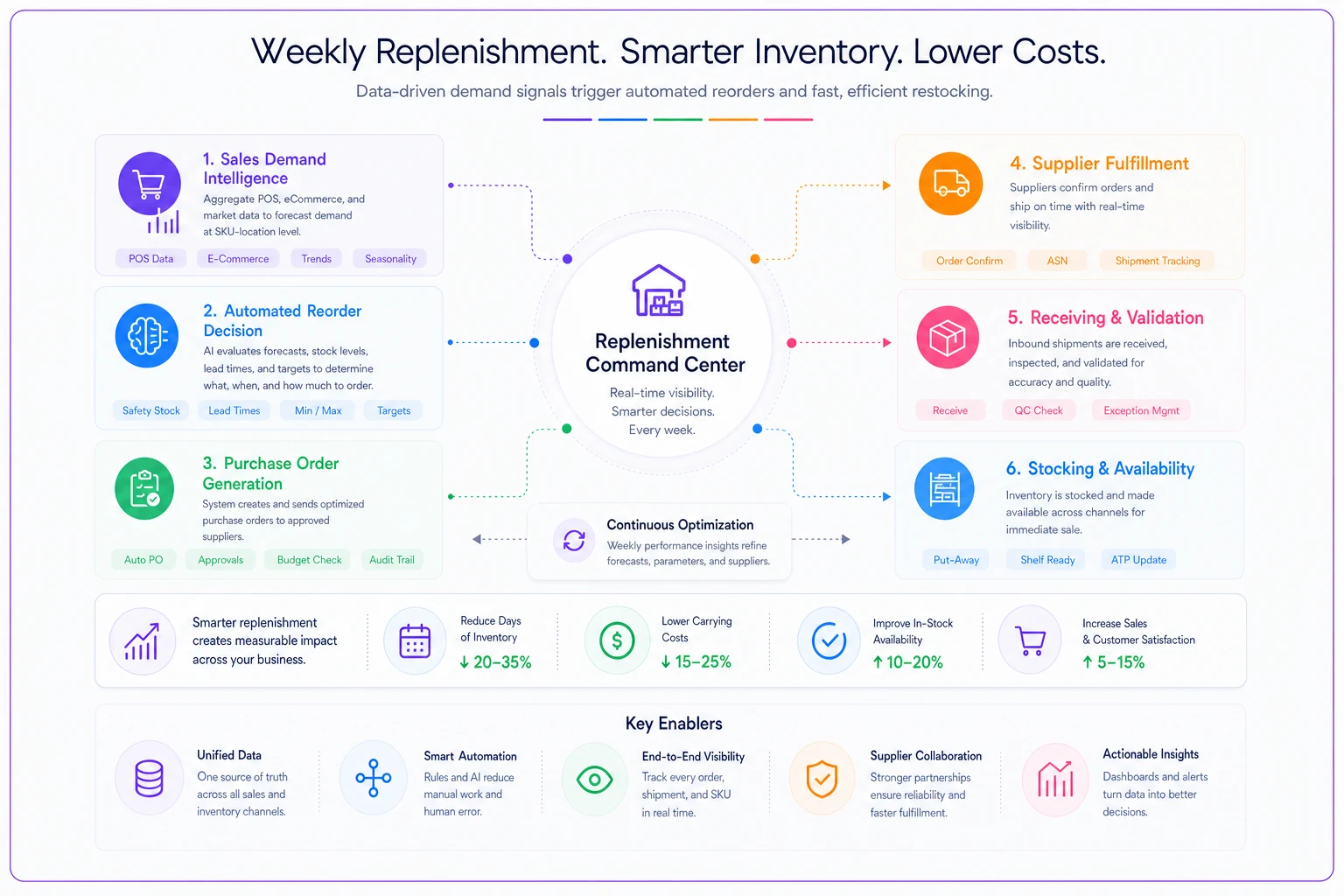

Moving from monthly to weekly replenishment cycles

The math is straightforward, but the operational change is hard. If you order monthly, you're carrying roughly 15 days of average inventory. Order weekly, you carry around 3–4 days. At 24% annual carrying cost, that difference adds up fast.

What nobody mentions: the setup cost to enable weekly ordering often kills the savings unless you automate the process.

Here's a quick workflow to illustrate the steps involved in moving to weekly replenishment.

Manual purchasing workflows can't handle four times as many orders efficiently. The labor cost of processing that volume wipes out the carrying cost savings. This is where investing in operational software actually pencils out—automated reordering based on real-time stock levels and demand patterns makes frequent ordering feasible.

A pet supply distributor switched from monthly to weekly ordering on their top 200 SKUs. The carrying cost savings came to around $2,100 monthly. But they only got there after implementing an AI-powered operational platform that automated purchase order generation based on sales velocity and current stock. Without the automation, the administrative burden would have eaten the savings whole.

There's also a side benefit: weekly ordering naturally pushes you toward SKU rationalization to cut carrying costs. You can't efficiently manage weekly orders across 5,000 SKUs. You focus on what actually moves, which compounds the carrying cost reduction.

Immediate moves versus structural changes

Getting from "we need to cut carrying costs" to actually doing it requires thinking in phases. The sequencing matters as much as the actions themselves—liquidating dead stock first gives you immediate breathing room and proves out the cash recovery concept internally before you start asking suppliers to restructure agreements.

| **Timeframe** | **Action** | **Typical Impact** | **Implementation Effort** |

|---|---|---|---|

| This week | Liquidate dead stock | Free up $30k–100k | Few hours of analysis |

| Next 2 weeks | Renegotiate payment terms | 30–60 day float | Multiple supplier calls |

| Next month | Shift to weekly ordering (top SKUs) | 15–20% carrying cost reduction | System setup required |

| Next quarter | Implement VMI/consignment | 25–40% reduction in owned inventory | Contract negotiations |

| Next 6 months | Full SKU rationalization | 20–30% inventory reduction | Significant operational change |

Some of these overlap, and that's fine. The point is to avoid doing them all at once and creating operational chaos while your cash position is already under pressure.

When aggressive inventory cuts backfire

There's a temptation to slash inventory across the board when rates spike. That's usually a mistake that costs more than it saves.

A sporting goods retailer panicked when their credit line hit 9.5% and cut inventory by 40% across all categories. They lost $180k in sales over three months because they couldn't fulfill orders. The lost margin exceeded the carrying cost savings by roughly 3x.

Smart inventory reduction is surgical. You protect availability on high-margin, fast-moving items while aggressively cutting slow-movers and duplicates. The goal is maximizing cash velocity, not minimizing inventory levels as a vanity metric.

Businesses that weather rate increases successfully tend to maintain—or even increase—inventory on their profit drivers while cutting everything else. They'd rather pay high carrying costs on inventory that turns 12 times per year than save a few points on items that turn twice.

Building variable-rate scenario models

Static planning doesn't work anymore. You need models that adjust as rates change.

Most small businesses can build something useful in a spreadsheet. Here's a practical way to structure it:

-

List your inventory categories and average values

-

Calculate current carrying costs at today's rates

-

Create scenarios for rates increasing 0.5%, 1%, and 2%

-

Identify trigger points where you'd need to act

The trigger points matter more than the precision of the calculations. At what rate does it make sense to drop a product line? When do you shift from ownership to consignment? What interest rate makes daily deliveries cheaper than holding safety stock?

A wholesale beauty supplier built this model and found their breakeven point for maintaining their full catalog was 9% on their credit line. Above that, they needed to cut 20% of SKUs or risk negative cash flow. They started the reduction process at 8.5%, giving themselves runway to execute properly instead of panic-cutting when they hit the wall.

Having that number in advance changes everything about how you make decisions under pressure.

Software as a force multiplier during transitions

The businesses navigating this rate environment well aren't just cutting costs—they're getting smarter about operations. Manual inventory management that worked fine at 15% carrying costs becomes a liability at 25%.

AI-assisted operational platforms make a real difference here. Not as a magic fix, but as infrastructure that enables strategies that wouldn't be feasible to run manually. Weekly reordering, dynamic safety stock adjustments, automated supplier scorecards—these require either significant staff time or intelligent automation.

The math is straightforward enough: if operational software runs $500 per month but enables inventory reductions that save $2,000 in monthly carrying costs, it pays for itself four times over. Factor in reduced stockouts, better supplier negotiations, and freed-up staff time, and the ROI compounds quickly.

The real value isn't the software itself—it's being able to execute aggressive inventory strategies without dropping details. You can cut deeper and move faster when systems are catching what humans miss during transitions.

What to do in the next 30 days

The Fed's signal about future rate increases means this isn't a temporary adjustment. According to the official Fed release, this rate environment is likely to persist for at least another year. The businesses that adapt now will have a real advantage over those waiting for rates to fall.

Start with the 72-hour assessment. Walk your inventory this week, identify what would go if you needed emergency cash, and actually move it. Convert dead stock to working capital while there's still a market for it.

Then pull your real carrying cost number—not just your interest rate, but the full cost including warehouse, insurance, obsolescence, and handling. Once you see the real percentage, every inventory decision looks different.

The businesses holding up in this environment aren't necessarily the ones with the best credit terms. They're the ones who adapted fastest, cut the right items, and built operations designed for expensive money. The adjustment is painful—but bleeding cash through carrying costs while competitors get lean is worse.

Ready to optimize your inventory operations?

Join 2,000+ businesses using Listoly to reduce stockouts, save time, and improve order accuracy.